First-Time Home Buyer Guide India 2026: Complete Checklist & 7 Mistakes to Avoid

As a first-time home buyer in India, you need a 750+ CIBIL score, 20-30% down payment, and EMI below 35% of income. Start by getting pre-approved 3-6 months before property hunting. Claim PMAY subsidy up to ₹2.67 lakh if eligible.

Not sure how much you can borrow? Calculate your eligibility based on salary and CIBIL score in 10 seconds.

Check My Home Loan EligibilityBuying your first home in India is both exciting and overwhelming. Unlike experienced buyers, first-timers often make costly mistakes that can cost lakhs of rupees and years of financial stress. This comprehensive guide walks you through every step—from checking your credit score 6 months before applying to moving into your dream home.

A home loan (also called housing loan or mortgage) is a secured loan provided by banks and housing finance companies (HFCs) to help you purchase residential property. The property itself serves as collateral, which is why home loans offer lower interest rates (8.5%-9.5% in 2026) compared to personal loans (10-15%).

As a first-time buyer, you have access to special benefits like PMAY subsidy up to ₹2.67 lakh, relaxed eligibility criteria from some lenders, and generous tax deductions under the old tax regime. However, 68% of first-time buyers overpay due to lack of research—this guide ensures you're not one of them.

Types of Home Loans

- Home Purchase Loan: For ready-to-move-in properties

- Home Construction Loan: Building on your own land

- Home Improvement Loan: Renovation of existing property

- Balance Transfer: Shifting to lower interest rate bank

Key Features for First-Timers

- LTV Ratio: Borrow up to 90% (₹30L property)

- Interest Rate: 8.50% - 9.50% p.a. (Feb 2026)

- Tenure: 5 to 30 Years (choose 15-20 yrs)

- Tax Savings: Up to ₹3.5L/year (old regime)

- PMAY Subsidy: Up to ₹2.67L (if eligible)

Your first home is within reach with proper planning and guidance.

Most home loan guides are written for all buyers. But first-timers face unique challenges that experienced buyers don't:

Challenges First-Timers Face

- ❌No credit history or low CIBIL score

- ❌Don't know how much they can truly afford

- ❌Underestimate total upfront costs (30-35%)

- ❌Fall for "low EMI" traps (30-year tenure)

- ❌Miss out on PMAY subsidy (₹2.67L free money)

What This Guide Covers

- ✅6-month preparation timeline (build credit score)

- ✅Pre-approval process (before property hunting)

- ✅PMAY eligibility and application steps

- ✅Co-borrower strategy (double tax benefits)

- ✅7 costly mistakes with real case studies

💡 Pro Tip: Bookmark this page and follow the timeline section. Checking off each step will ensure you don't miss critical deadlines or benefits.

Your 6-Month Timeline to First Home

Don't wait until you find your dream property. Start preparing 6 months in advance to get the best rates and avoid delays.

Month -6: Foundation Building

- Check CIBIL score: Get free report from cibil.com. Target 750+.

- Fix credit issues: Pay all outstanding dues, dispute errors, reduce credit utilization below 30%.

- Start saving: Open dedicated account for down payment. Automate ₹20-30k/month transfers.

- Research property rates: Track prices in target localities using MagicBricks, 99acres.

Goal: CIBIL 750+, ₹5-10L saved

Month -3: Pre-Approval Stage

- Calculate affordability: EMI should be max 35% of monthly income. Use our calculator below.

- Gather documents: Salary slips (6mo), Form 16, bank statements, PAN, Aadhaar.

- Apply for pre-approval: Submit to 3-4 banks/HFCs. Receive sanction letters in 5-7 days.

- Check PMAY eligibility: Income below ₹18L? Property below ₹45L? Apply for subsidy.

Goal: Pre-approval from 3 lenders, know exact loan amount

Month -1: Property Hunting

- Visit properties: Shortlist 5-7 options. Check location, builder reputation, possession date.

- Verify legal documents: Title deed, NOC, approved plans, occupancy certificate.

- Negotiate price: Show pre-approval letter. Ask for 5-10% discount or free furnishings.

- Book property: Pay token amount (₹50k-1L). Sign sale agreement within 15 days.

Goal: Property finalized, agreement signed

Current Month: Loan Finalization

- Submit full documentation: Property papers to bank for legal/technical verification.

- Bank verification: Wait 15-20 days for legal clearance and valuation report.

- Final sanction: Receive approved loan amount, sign agreement. Buy home insurance (mandatory).

- Registration & Disbursement: Pay stamp duty (5-7%), register property. Bank transfers funds to seller.

Goal: Keys in hand, EMI starts next month 🎉

Reality Check: Most first-timers rush into property hunting without pre-approval. This leads to losing dream properties to buyers with financing ready. Follow this timeline religiously.

Pre-Approval: Your Secret Weapon

Pre-approval is a preliminary assessment where banks tell you exactly how much they'll lend you before you start property hunting. It's valid for 60-90 days and gives you massive negotiating power with sellers.

| Feature | Pre-Approval | Final Approval |

|---|---|---|

| When to Apply | Before property hunting | After selecting property |

| Documents Needed | Basic (Income proof, CIBIL) | Complete (+ Property papers) |

| Timeline | 3-7 days | 15-30 days |

| Validity | 60-90 days | Until disbursement |

| Commitment | Soft (subject to verification) | Hard (guaranteed funds) |

- ✅Know exact budget: No time wasted on unaffordable properties

- ✅Negotiate better: Sellers take you seriously with pre-approval letter

- ✅Move fast: Beat other buyers who need weeks for loan approval

- ✅Rate lock: Some banks lock interest rate at pre-approval stage

Salaried Employees:

- • Last 3 months salary slips

- • Last 3 months bank statements

- • PAN card + Aadhaar card

- • Employment letter (optional)

Self-Employed:

- • Last 2 years ITR with computation

- • Last 6 months bank statements

- • Business registration proof

- • PAN + Aadhaar

Common Pre-Approval Mistakes

- 1. Applying to only 1 bank: Get quotes from 3-4 lenders to compare rates.

- 2. Not reading fine print: Check processing fees, pre-approval validity period.

- 3. Overestimating budget: Pre-approval shows max loan, not what you should borrow (keep EMI < 35% income).

Ready for pre-approval? Calculate your eligibility and apply to top 3 banks instantly.

Get Pre-Approval EstimatesPMAY Subsidy: Get Up to ₹2.67 Lakh Free

Pradhan Mantri Awas Yojana (PMAY) is the government's flagship scheme offering interest subsidy to first-time home buyers. If eligible, you receive a direct upfront subsidy that reduces your loan principal—essentially free money that saves lakhs over your loan tenure.

| Category | Annual Income | Max Property Value | Interest Subsidy | Max Subsidy Amount |

|---|---|---|---|---|

| EWS/LIG | Up to ₹6 Lakh | ₹45 Lakh | 6.50% | ₹2.67 Lakh |

| MIG-I | ₹6 - 12 Lakh | ₹45 Lakh | 4.00% | ₹2.35 Lakh |

| MIG-II | ₹12 - 18 Lakh | ₹45 Lakh | 3.00% | ₹2.30 Lakh |

* Subsidy calculated on loan amount up to ₹6L (EWS/LIG), ₹9L (MIG-I), or ₹12L (MIG-II) for tenure of 20 years or actual tenure, whichever is lower.

- First-time buyer: You or family shouldn't own any pucca house in India

- Income limit: Annual family income below ₹18 lakh

- Property value: Not exceeding ₹45 lakh

- Carpet area: Max 60 sqm (metros), 90 sqm (non-metros)

- No prior subsidy: Haven't availed PMAY benefit before

- Women ownership: Property in woman's name (sole or joint) gets priority

- Check eligibility: Visit pmaymis.gov.in and use eligibility calculator

- Get Aadhaar verified: Link Aadhaar with bank account (mandatory)

- Apply online: Fill PMAY-U application on portal or through bank

- Choose PMAY-linked lender: Not all banks offer PMAY. Check approved list

- Submit documents: Income proof, property papers, Aadhaar, PAN

- Sanction letter: Bank approves loan with PMAY subsidy mentioned

- Upfront subsidy: Government credits subsidy directly to your loan account within 2-3 months

Profile

PMAY Impact

| Without PMAY | ₹32,00,000 |

| PMAY Subsidy (4% on ₹9L) | - ₹2,35,000 |

| Effective Loan Amount | ₹29,65,000 |

| EMI Reduction | ↓ ₹2,000/month |

| Total Savings (20 yrs) | ₹7.8 Lakh |

💡 Pro Tip: Priya also gets tax benefits on the reduced EMI. Combined with PMAY, she saves over ₹10 lakh during the loan tenure!

Common PMAY Rejections

- 1. Property too expensive: ₹45L limit is strict. Even ₹46L property is ineligible.

- 2. Already own property: Even ancestral property in village disqualifies you.

- 3. Income proof mismatch: Showing ₹18L+ income leads to automatic rejection.

- 4. Applied through non-PMAY bank: Check pmaymis.gov.in for approved lender list.

Home Loan Eligibility for First-Timers (2026)

Understanding eligibility is crucial for first-time buyers who often lack credit history. Here's what major Indian lenders evaluate:

1. Age Requirements

| Bank/HFC | Min Age | Max Age at Maturity | First-Timer Friendly? |

|---|---|---|---|

| SBI, HDFC, ICICI | 21 years | 70 years | ✅ Yes |

| Axis Bank | 21 years | 70 years | ✅ Yes |

| PNB Housing | 21 years | 75 years | ✅ Yes |

| LIC Housing | 21 years | 70 years | ✅ Most Lenient |

2. Income & Credit Score (First-Timer Considerations)

- Min Salary: ₹25k - ₹40k/month (varies by city)

- Business Income: ₹2L+ Annual (with 3 years ITR)

- Work Experience: Min 2 years total, 1 year in current company

- First-Timer Tip: Add parent/spouse as co-applicant to boost eligibility

- 750+: Excellent rate (8.5%) - Easy approval

- 700-749: Good rate (8.75%) - Standard approval

- 650-699: Average (9.5%) - Requires co-borrower

- <650 or No History: High risk - Apply to HFCs, add co-borrower with good score

First-Timers Without Credit History: Your Options

Short-term (3-6 months before applying):

- Get secured credit card against FD

- Use it for small purchases, pay full amount on time

- This builds 700+ score in 6 months

Applying now without history:

- Add co-applicant with 750+ score (parent/spouse)

- Apply to HFCs (LIC Housing, PNB Housing more lenient)

- Provide alternative proof: rent receipts, utility bills

Co-Borrower Strategy: Double Your Benefits

Adding a co-borrower (spouse, parent, or sibling) to your home loan can double your tax benefits, increase loan eligibility by 50-100%, and improve approval chances if you have limited credit history. However, it comes with shared liability and impacts both credit scores.

| Role | Loan Liability | Property Rights | Tax Benefits | Best For |

|---|---|---|---|---|

| Co-Borrower | ✅ Yes (Joint) | ✅ Yes | ✅ Yes (Both) | Spouse, parent with income |

| Co-Owner | ❌ No | ✅ Yes | ❌ No | Adding family member to deed |

| Guarantor | ⚠️ Only if you default | ❌ No | ❌ No | Low credit score backup |

- ✅Higher eligibility: Combined income = 50-100% more loan amount

- ✅Double tax benefits: Each co-borrower claims ₹3.5L = ₹7L total/year

- ✅Better interest rate: Good co-borrower CIBIL improves your rate

- ✅Easy approval: Compensates for your limited credit history

- ✅Lower stamp duty: Many states offer 1-2% discount if woman is co-owner

- ❌Joint liability: If you default, co-borrower's CIBIL also tanks

- ❌Affects co-borrower's loan capacity: They can't buy another property easily

- ❌Property ownership: Co-borrower must be co-owner (can't remove later)

- ❌Relationship risk: Future disputes over property ownership

- ❌Exit hassles: Removing co-borrower requires full refinancing

Scenario A: Rahul Alone

Scenario B: Rahul + Neha (Co-Borrower)

💰 Result: By adding Neha, Rahul can buy a ₹58L property instead of ₹35L, and they save an extra ₹3.5L/year in taxes. Over 20 years, that's ₹70 lakh in additional tax savings!

Who Should You Add as Co-Borrower?

✅ Best Choice: Spouse

- • Natural co-owner

- • Double tax benefits

- • Lower stamp duty (women)

- • No future ownership disputes

⚠️ Good Choice: Parent

- • If single/unmarried

- • Parent has steady income

- • Consider inheritance issues

- • Exit clause if you marry later

❌ Risky: Sibling/Friend

- • High ownership dispute risk

- • Complex family dynamics

- • Hard to exit arrangement

- • Use only as last resort

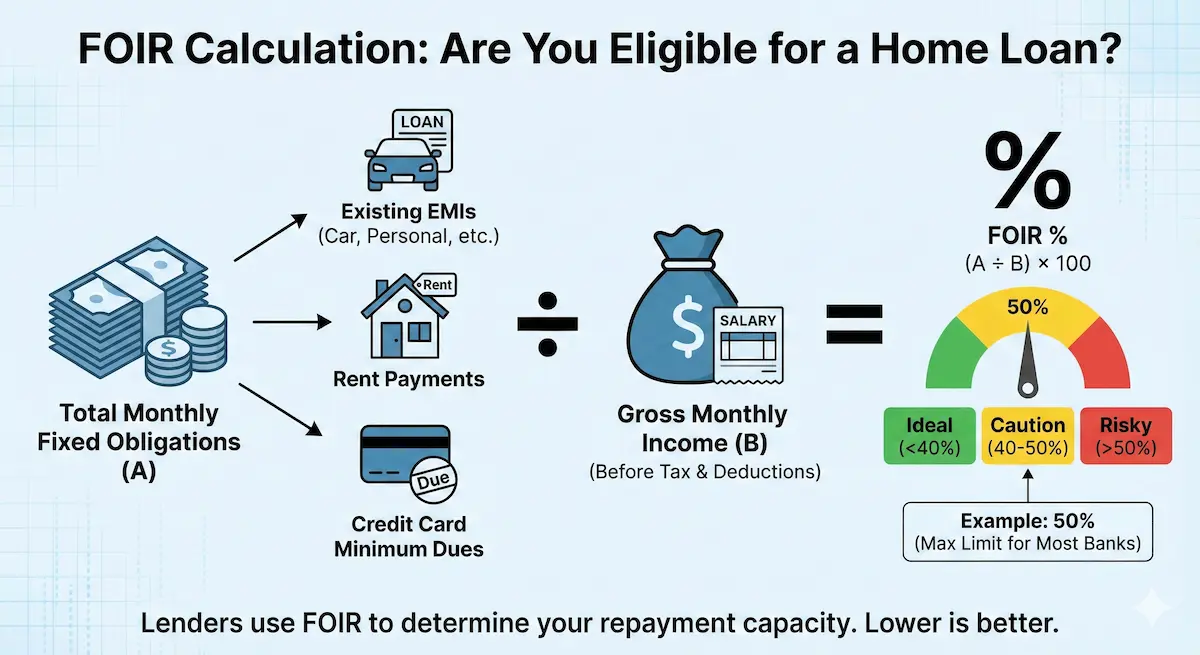

FOIR: The Make-or-Break Number

FOIR (Fixed Obligations to Income Ratio) is the percentage of your monthly income that goes toward fixed financial obligations like EMIs and rent. Banks use FOIR to determine if you can actually afford the home loan EMI without defaulting.

For first-time buyers, understanding FOIR is critical because many overestimate their borrowing capacity, leading to rejection or financial stress post-approval.

Income Side

Obligations Side

FOIR = (₹48,000 / ₹80,000) × 100 = 60%

This is at the upper limit. Banks prefer 50-55% FOIR for first-timers.

| Lender Type | Max FOIR Allowed | Your Take-Home | First-Timer Advice |

|---|---|---|---|

| Public Sector Banks | 50% | 50% | Strictest criteria |

| Private Banks | 50-55% | 45-50% | Standard for most |

| HFCs (LIC, PNB) | 55-60% | 40-45% | More lenient, but risky |

- Can't save: Living paycheck to paycheck

- No emergency fund: Vulnerable to income shocks

- Delayed EMIs: High default risk

- High stress: Mental health impact

- Close personal loans: Pay off high-interest debts first

- Clear credit cards: Reduces monthly obligations

- Add co-borrower: Increases combined income

- Wait for increment: Delay by 3-6 months if needed

First-Timer Tip: Aim for 40-45% FOIR, not the maximum 60%. This gives you breathing room for unexpected expenses (medical, car repairs, weddings) and lets you save for prepayment or investments.

Down Payment Rules: Budget for 30-35%

Many first-time buyers think down payment = 20% of property value. Wrong! You need to budget for 30-35% of total property cost upfront when factoring in stamp duty, registration, and other charges.

| Property Value | Max LTV (Bank Loan) | Your Down Payment | Example |

|---|---|---|---|

| Up to ₹30 Lakh | 90% | 10% | ₹25L property = ₹2.5L down payment |

| ₹30L - ₹75L | 80% | 20% | ₹50L property = ₹10L down payment |

| Above ₹75 Lakh | 75% | 25% | ₹1Cr property = ₹25L down payment |

| Property Value | ₹50,00,000 | Base cost |

| Down Payment (20%) | ₹10,00,000 | To seller |

| Stamp Duty (6% avg) | ₹3,00,000 | State govt |

| Registration Charges (1%) | ₹50,000 | Sub-registrar |

| Home Loan Processing Fee (0.5%) | ₹25,000 | Bank charges |

| Legal/Valuation Charges | ₹15,000 | Verification |

| Home Insurance (First year) | ₹10,000 | Mandatory |

| Total Upfront Cost | ₹14,00,000 | 28% of property |

⚠️ Reality Check: For a ₹50L property, you need ₹14L cash upfront, not just ₹10L. Plus keep ₹2-3L extra for furnishing and emergencies. Total savings needed: ₹17L minimum.

💡 First-Timer Saving Strategy:

- • Start saving 20-25% of salary in dedicated account 2 years before

- • Use recurring deposits/liquid funds (don't lock in fixed deposits)

- • Negotiate stamp duty discount if property in woman's name (1-2% in many states)

- • Ask bank to waive processing fee during festive offers (saves ₹25-50k)

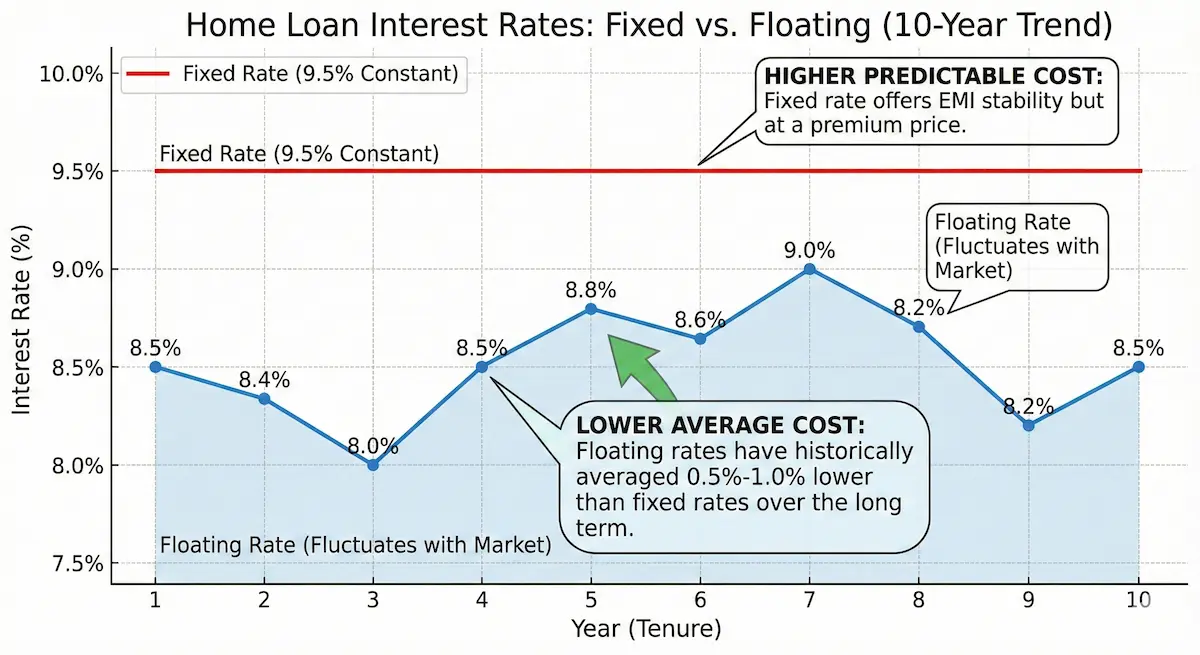

Fixed vs Floating: Which Rate for First-Timers?

Interest rate changes with RBI Repo Rate. Most popular choice in India.

✅ Choose if: 20+ year tenure, can handle EMI fluctuations, want flexibility to prepay

Constant rate for 3-5 years, then converts to floating.

⚠️ Choose if: Tight budget, can't afford ₹1-2k EMI increase, 5-10 year tenure only

First-Timer Mistake: Choosing Fixed Rate

82% of Indian borrowers choose floating rate. Fixed rates are popular only during high inflation periods. In Feb 2026, with RBI expected to cut rates, floating is the clear winner.

Example: Raghav took ₹40L fixed at 9.8% in 2024. RBI cut rates by 0.75% in 2025-26. His friend with floating rate now pays ₹2,300 less EMI per month. Raghav can't prepay without 3% penalty (₹1.2L loss).

Tax Benefits: Save ₹3.5 Lakh/Year (Old Regime)

⚠️ CRITICAL UPDATE: Section 80EEA Expired

Section 80EEA (additional ₹1.5 lakh deduction for first-time buyers) expired on March 31, 2022. It is NO LONGER AVAILABLE for loans sanctioned after this date.

Maximum tax benefit available now: ₹3.5 lakh/year (₹1.5L under 80C + ₹2L under 24b). Many websites still show outdated ₹5L benefit—ignore them.

- • Includes stamp duty & registration (one-time)

- • Principal portion of EMI qualifies

- • Property shouldn't be sold within 5 years (clawback)

- • Shared with PPF, ELSS, LIC premiums (₹1.5L combined limit)

- • Self-occupied property: Max ₹2L

- • Let-out property: Full interest deductible (no limit)

- • Construction must complete within 5 years of loan

- • Pre-construction interest deducted over 5 years (1/5th annually)

| Feature | Old Regime | New Regime |

|---|---|---|

| Home Loan Benefits | ✅ ₹3.5L/year | ❌ Zero |

| Tax Slabs | 10%, 20%, 30% | 5%, 10%, 15%, 20%, 30% |

| Other Deductions | PPF, ELSS, NPS, etc. | Only Standard ₹50k |

| Best for Home Buyers? | ✅ Yes (if income < ₹15L) | Only if income > ₹20L |

* For ₹12L income with ₹40k EMI, old regime saves ₹1.05L more in taxes annually. Use our Income Tax Calculator to compare.

First-Timer Tip: Stay in old tax regime for first 5-7 years of home loan. Interest component is highest in early years (₹2L+ annually), maximizing your 24(b) benefit. Switch to new regime later if your income crosses ₹20L and deductions reduce.

7 Costly Mistakes First-Time Buyers Make

Learn from others' expensive mistakes. These 7 errors cost first-time buyers lakhs of rupees and years of stress.

Not Getting Pre-Approved Before Property Hunting

The Mistake: Falling in love with ₹60L property, then discovering you're eligible for only ₹40L loan.

Real Story: Anjali spent 3 months searching Mumbai properties, paid ₹1L token for ₹58L flat. Bank approved only ₹35L. Lost token money + dream home.

Solution: Get pre-approval from 3 banks BEFORE property hunting. Know exact budget. Show pre-approval letter to negotiate 5-10% discount with seller.

💸 Cost: ₹1L+ token loss + 3 months wasted

Underestimating Total Upfront Costs

The Mistake: Saving only 20% down payment, forgetting stamp duty (5-7%), registration (1%), furnishing (₹3-5L).

Real Story: Rohit saved ₹10L for ₹50L flat. Shocked by ₹3L stamp duty + ₹50k registration + ₹4L furnishing. Had to take personal loan at 14% for remaining ₹7.5L.

Solution: Budget 35% of property value upfront (not 20%). For ₹50L property: ₹10L down payment + ₹3L stamp duty + ₹50k registration + ₹25k bank charges + ₹3L furnishing = ₹17L total.

💸 Cost: ₹1-2L extra in personal loan interest (14% vs 8.5%)

Choosing Maximum Tenure to Lower EMI

The Mistake: Choosing 30-year tenure for "affordable" ₹30k EMI instead of 20-year ₹38k EMI.

Real Story: Priya took ₹40L for 30 years (EMI ₹33k). Friend Neha took same loan for 20 years (EMI ₹41k). After 20 years, Priya still owes ₹18L while Neha is debt-free. Priya will pay ₹78L total interest vs Neha's ₹51L.

Solution: Choose 15-20 year tenure. If EMI unaffordable, buy cheaper property instead. Your salary will grow—prepay aggressively in years 3-7 to reduce tenure.

💸 Cost: ₹27L extra interest over loan life

Not Checking CIBIL Score Before Applying

The Mistake: Applying with 640 score, getting rejection that further damages score to 610.

Real Story: Arun applied to 4 banks with 655 score. All rejected (multiple inquiries dropped score to 620). Waited 8 months to rebuild score to 730, then approved but at 9.25% instead of 8.5%.

Solution: Check CIBIL 6 months before applying. If <700, spend 6 months improving: pay all dues, reduce credit utilization to <30%, dispute errors. Target 750+ before applying.

💸 Cost: 0.75% higher rate = ₹2.8L extra interest on ₹40L/20yr loan

Skipping Property Legal Verification

The Mistake: Trusting builder's documents without independent lawyer verification.

Real Story: Meera bought ₹55L flat, bank approved loan. After 1 year, discovered property had pending litigation. Can't sell or rent. Stuck paying EMI for unusable property.

Solution: Hire property lawyer (₹10-15k) to verify: title deed chain, encumbrance certificate, NOC from authorities, approved building plans, occupancy certificate. Don't rely only on bank's verification.

💸 Cost: Entire ₹55L investment at risk + legal fees ₹2-5L

Missing Out on PMAY Subsidy

The Mistake: Not applying for PMAY despite being eligible, losing ₹2.35L free subsidy.

Real Story: Karan bought ₹42L flat with ₹10L income. Didn't know about PMAY. Friend told him 2 years later—too late to apply retroactively. Lost ₹2.35L subsidy forever.

Solution: Check PMAY eligibility on pmaymis.gov.in BEFORE loan approval. Income <₹18L + Property <₹45L + First home = Apply immediately. Choose PMAY-approved bank.

💸 Cost: ₹2.35L direct subsidy lost + ₹5.5L interest savings over 20 years

Not Comparing Multiple Banks

The Mistake: Going with employer tie-up bank at 9.15% without comparing other banks offering 8.65%.

Real Story: Vikram took ₹45L at 9.15% from HDFC (employer tie-up). Colleague got 8.65% from SBI. 0.5% difference = ₹4,200 higher EMI for Vikram. Over 20 years, he pays ₹10L extra.

Solution: Get quotes from minimum 4 banks (2 PSU + 2 private). Compare: interest rate, processing fee, prepayment charges, tenure flexibility. Negotiate using competitor quotes.

💸 Cost: ₹10L+ extra interest due to 0.5% higher rate

Avoiding These 7 Mistakes Saves: ₹1L token + ₹2L personal loan interest + ₹27L excess tenure interest + ₹2.8L rate difference + ₹5L legal risk + ₹2.35L PMAY + ₹10L comparison = ₹50+ Lakh over loan life

Complete Application Checklist for First-Timers

Phase 1Pre-Application (6 Months Before)

- Check CIBIL Score: Get free report, target 750+. Dispute errors immediately.

- Calculate Affordability: EMI should be max 35% of income. Use calculator to find budget.

- Start Saving Down Payment: Target 30-35% of property value (not just 20%).

- Build Credit History: If no credit card, get secured card and use responsibly for 6 months.

- Close Unnecessary Loans: Pay off personal loans, reduce credit card dues to improve FOIR.

- Research PMAY Eligibility: Check if income <₹18L and property will be <₹45L.

Phase 2Application Stage (3 Months Before)

- Gather Income Documents: Salaried: 6 months salary slips, Form 16, bank statements. Self-employed: 3 years ITR, audited financials.

- Gather KYC Documents: PAN card, Aadhaar card, passport, voter ID, passport size photos (10 copies).

- Apply for Pre-Approval: Submit to 3-4 banks (mix of PSU and private). Get sanction letters.

- Decide on Co-Borrower: Add spouse/parent if needed for higher eligibility or better rate.

- Compare Final Offers: Interest rate, processing fee, tenure options, prepayment terms. Negotiate.

- Property Hunting: Visit 5-7 properties, check location, builder reputation, legal documents.

Phase 3Property Selection (1 Month Before)

- Verify Legal Documents: Title deed, encumbrance certificate, approved building plans, NOC, occupancy certificate.

- Hire Property Lawyer: Independent verification (₹10-15k). Don't rely only on bank's check.

- Negotiate Price: Show pre-approval letter, ask for 5-10% discount or free furnishings.

- Pay Token Amount: ₹50k-1L. Get token receipt, sign MOU (Memorandum of Understanding).

- Submit Property Papers to Bank: Sale agreement, NOC, approved plans for bank's legal/technical verification.

Phase 4Disbursement & Possession (Current Month)

- Wait for Bank Verification: Legal + Technical check takes 15-20 days. Follow up weekly.

- Receive Final Sanction Letter: Confirms loan amount, interest rate, tenure. Review carefully.

- Sign Loan Agreement: Read all terms, check prepayment clauses, processing fee, late payment charges.

- Buy Home Loan Insurance: Mandatory by most banks. Shop for best rates (₹8-12k/year).

- Register Property: Pay stamp duty (5-7%) + registration (1%) at sub-registrar office. Get registered sale deed.

- Bank Disburses Funds: Directly to seller's account. Collect keys from builder/seller.

- Collect Original Documents: Bank holds till loan repaid. You get photocopy + acknowledgement receipt.

- Set Up Auto-Debit EMI: Link bank account, set EMI date after salary credit. Never miss EMI (damages CIBIL).

Post-Possession: Next Steps

- • Update address in Aadhaar, PAN, bank, employer (within 3 months)

- • Apply for PMAY subsidy if eligible (within 6 months of disbursement)

- • Keep all receipts for tax filing (stamp duty, registration, EMI statements)

- • Start prepayment from Year 2-3 onwards (saves maximum interest)

- • Review home insurance annually, switch if better rates available

Frequently Asked Questions (First-Time Buyers)

- Start 6 months early: Build CIBIL score to 750+, save 35% of property value, get pre-approved before hunting.

- PMAY is free money: If income <₹18L and property <₹45L, apply for up to ₹2.67L subsidy. Don't miss this.

- Co-borrower doubles benefits: Add spouse to claim ₹7L tax benefits/year instead of ₹3.5L. Plus increase eligibility by 50-100%.

- Choose floating rate: 95% of Indians choose floating. Lower rate (8.5%), zero prepayment charges, benefits from RBI cuts.

- Keep EMI <35% of income: Not the bank's max 60%. You need buffer for emergencies, savings, lifestyle expenses.

- Choose 15-20 year tenure: Not 25-30 years. You'll pay 2-3x property value in interest. Buy cheaper property if needed.

- Old tax regime for home buyers: Save ₹3.5L/year vs zero in new regime. Switch to new only if income >₹20L later.

- Compare 4+ banks: 0.5% rate difference = ₹10L over 20 years. Get quotes from 2 PSU + 2 private banks minimum.

Ready to Start Your Home Buying Journey?

Calculate your exact eligibility, compare banks, and get pre-approval estimates in 2 minutes.

Free • No registration • Instant results • Compare top banks

Written by Fincado Research Team

Expert financial analysts specializing in personal finance, home loans, and tax planning for Indian consumers. Our team has helped over 50,000 first-time buyers navigate the home loan process successfully.

Found this guide helpful? Share it with friends planning to buy their first home:

Disclaimer

This guide is for educational purposes only and should not be considered financial advice. Home loan interest rates, eligibility criteria, PMAY schemes, and tax laws are subject to change. Section 80EEA expired on March 31, 2022, and is no longer available. Please consult with a certified financial advisor, chartered accountant, or property lawyer before making any financial or property decisions. Actual loan approval and terms depend on individual circumstances, bank policies, credit profile, and property verification. Information last updated: Feb 2026.