The Complete Home Loan Guide 2026: Eligibility, Tax Benefits & Application Process

Home loans in India cost 8.5-9.5% interest and require a 750+ CIBIL score for best rates. You can borrow up to 90% of property value with repayment over 5-30 years. Tax benefits apply only under the old tax regime.

*Only under old tax regime (80C + 24b)

Want to know your exact EMI? Calculate loan affordability based on your salary in 10 seconds.

Calculate My Home Loan EMIBuying your first home in India is one of the biggest financial decisions you'll ever make, and choosing the right Home Loan can save you lakhs of rupees over the loan tenure. This comprehensive guide covers everything from CIBIL score requirements and tax benefits to the complete application process and hidden charges, helping you make an informed decision before signing on the dotted line.

Whether you're a first-time home buyer or looking to refinance, understanding home loan eligibility criteria, tax deductions under Section 80C and 24(b), the difference between RLLR vs MCLR, and the step-by-step application process will put you in control of your home-buying journey. Also learn about stamp duty variations across states and smart prepayment strategies.

Secure your dream home with the right loan strategy.

What is a Home Loan?

A home loan (also called housing loan or mortgage) is a secured loan provided by banks and housing finance companies (HFCs) to help you purchase, construct, renovate, or extend residential property. The property itself serves as collateral until the loan is fully repaid.

Key Components

- Principal Amount: Total loan amount borrowed from the bank.

- Interest Rate: Cost of borrowing (fixed or floating), currently 8.5-9.5% p.a.

- Tenure: Repayment period ranging from 5 to 30 years.

- EMI: Equated Monthly Installment (Principal + Interest).

- LTV Ratio: Loan-to-Value ratio, typically 75-90% of property value.

Types of Home Loans

- Purchase Loan: For buying ready-to-move-in property

- Construction Loan: For building on owned land

- Extension Loan: For expanding existing property

- Balance Transfer: Shifting loan to another bank

- Top-Up Loan: Additional loan on existing property

Step-by-Step Application Process

Understanding the home loan application journey helps you prepare better and avoid delays. Here's the complete process from pre-approval to disbursement.

Check Eligibility & Get Pre-Approval

Check your CIBIL score (minimum 700, ideally 750+) and calculate FOIR. Submit basic income documents to get a pre-approval letter indicating the loan amount you qualify for.

Timeline: 2-3 days | Validity: 60-90 days

Property Selection & Agreement

Choose your property, negotiate the price, and sign the sale agreement. Ensure the property has clear legal title and approved construction plans.

Key Check: Verify property documents, builder reputation, and municipal approvals

Submit Complete Documentation

Provide all required documents: income proof, bank statements, property papers, identity documents, and photographs. Ensure all documents are complete to avoid delays.

Pro Tip: Keep digital and physical copies organized in a folder. Missing documents cause 70% of application delays.

Property Verification (Legal & Technical)

Bank's legal team verifies property title, checks for encumbrances, and technical team assesses property valuation and construction quality.

Timeline: 7-15 days | Cost: ₹2,000-₹5,000 (technical valuation fee)

Final Sanction & Agreement Signing

Receive final sanction letter with approved loan amount, interest rate, and tenure. Sign the loan agreement and create Memorandum of Deposit of Title Deeds (MODT).

Timeline: 2-3 days after verification completion

Disbursement & Property Registration

Pay stamp duty and registration charges, complete property registration at sub-registrar office. Bank disburses loan amount to seller's account. EMI repayment starts from the next month.

Timeline: 1-2 days post registration | First EMI: Due within 30 days of disbursement

Total Timeline: Expect 15-30 days from application to disbursement if all documents are in order. Property verification is the longest step.

Eligibility Checklist

Before you apply, make sure you meet these critical eligibility parameters. Banks evaluate multiple factors to determine your loan amount and interest rate.

| Score Range | Eligibility Status | Interest Rate Impact |

|---|---|---|

| 750+ (Excellent) | Very high chance of approval | Lowest rates (8.5%-8.75%) |

| 700-749 (Good) | High chances of approval | Standard rates (8.75%-9.0%) |

| 650-699 (Fair) | Moderate chances | Higher rates (9.0%-9.5%) |

| Below 650 (Poor) | Low chances / Likely rejection | Very high rates or rejected |

FOIR measures what percentage of your monthly income goes towards debt obligations. Banks typically allow 50-60% FOIR.

FOIR Formula

Example Calculation

- Monthly Income: ₹80,000

- Existing Car Loan EMI: ₹10,000

- Proposed Home Loan EMI: ₹30,000

- FOIR = (10,000 + 30,000) / 80,000 × 100 = 50%

FOIR Thresholds

- Below 50%: Excellent eligibility

- 50-60%: Good eligibility

- 60-70%: Marginal, case-by-case

- Above 70%: Likely rejection

Tip: Close small personal loans or credit card dues before applying to improve your FOIR and get higher loan eligibility.

Age Requirements

| Minimum Age | 21 years |

| Maximum Age (at maturity) | 65-70 years |

| Salaried | Up to 60 years at retirement |

| Self-Employed | Up to 65-70 years |

Income Requirements

| Salaried (Metro) | ₹25,000+/month |

| Salaried (Non-Metro) | ₹15,000+/month |

| Self-Employed | ₹2-3 LPA net profit |

| Business Vintage | Minimum 2-3 years |

Calculate Your EMI

Adjust values to see instant results

Monthly EMI

₹0

Total Interest

₹0

Total Payment

₹0

Payment Breakdown

This calculator uses industry-standard FOIR (40-50%) and considers your credit score to estimate eligibility accurately. Open full calculator →

For Salaried Individuals

- Last 6 months' salary slips

- Form 16 (last 2 years)

- Last 6 months' bank statements (salary account)

- PAN card & Aadhaar card

- Property documents (sale agreement, builder NOC)

- Employment letter or offer letter

- Passport-size photographs

For Self-Employed

- ITR (last 2-3 years) with computation sheets

- Audited financial statements (P&L, Balance Sheet)

- Business proof (GST registration, Shop Act license)

- Last 12 months' bank statements (business account)

- PAN, Aadhaar & property documents

- Business continuity proof (2-3 years minimum)

- Passport-size photographs

Property Documents Required

- Sale agreement / Allotment letter

- Property title deed (last 13+ years)

- Encumbrance certificate

- Building approved plan

- NOC from builder/society

- Possession letter (if ready property)

- Occupancy certificate

- Property tax receipts

Pro Tip: Keep digital copies (scanned PDFs) ready in a single folder labeled "Home Loan Docs". This speeds up approval by 7-10 days and prevents back-and-forth requests from the bank.

Tax Benefits Under Old Tax Regime

Critical: Tax Regime Selection Matters!

The tax benefits mentioned below (Sections 80C, 24b, and 80EEA) are ONLY available under the old tax regime. The new tax regime introduced in FY 2020-21 does NOT allow these deductions. Before claiming home loan tax benefits, you must opt for the old tax regime when filing your ITR. Calculate which regime saves you more →

One of the biggest advantages of taking a home loan in India is the significant tax deductions available under the Income Tax Act, 1961 (if you choose the old tax regime).

| Section | Covers | Max Deduction | Eligibility |

|---|---|---|---|

| Section 80C | Principal Repayment | ₹1,50,000 | All borrowers (old regime only) |

| Section 24(b) | Interest on loan | ₹2,00,000 | Self-occupied property (old regime) |

| Section 80EEA EXPIRED | Additional Interest | ₹1,50,000 | No longer available (expired March 31, 2022) |

Important Update: Section 80EEA, which provided an additional ₹1.5 lakh deduction for first-time home buyers, applied ONLY to loans sanctioned between April 1, 2019, and March 31, 2022, for properties with stamp duty value up to ₹45 Lakhs. This benefit is no longer available for loans sanctioned after March 31, 2022.

Annual Deductions Available

| Principal Repayment (80C) | ₹1,50,000 |

| Interest Payment (24b) | ₹2,00,000 |

| Total Annual Deduction | ₹3,50,000 |

Tax Savings by Income Bracket

| Tax Bracket | Annual Savings | 20-Year Savings |

|---|---|---|

| 30% bracket (income above ₹15L) | ₹1,05,000 | ₹21,00,000 |

| 20% bracket (₹10-15L) | ₹70,000 | ₹14,00,000 |

| 10% bracket (₹5-10L) | ₹35,000 | ₹7,00,000 |

When you take a joint home loan with a co-borrower (spouse, parent, sibling), BOTH individuals can claim independent deductions under Section 80C and Section 24(b), provided both are co-owners of the property. This effectively doubles the total tax benefit available.

Joint Loan Tax Math

Single Borrower:

- 80C: ₹1.5 lakh

- 24(b): ₹2 lakh

- Total: ₹3.5 lakh/year

Joint Borrowers (Both Co-owners):

- Borrower 1: ₹3.5 lakh

- Borrower 2: ₹3.5 lakh

- Total: ₹7 lakh/year 🎉

Pro Tip: Ensure both co-borrowers contribute to EMI payments from their respective bank accounts to claim individual deductions. Keep payment proofs for ITR filing.

Should you choose old or new tax regime? Calculate your tax liability under both regimes considering home loan deductions.

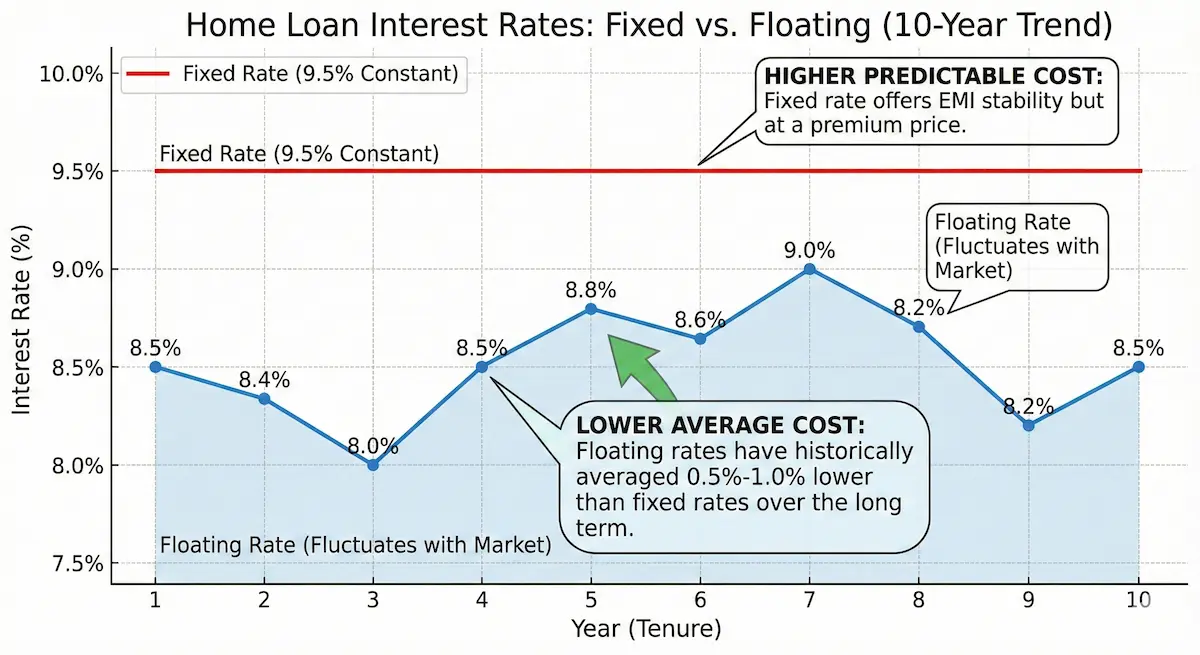

Compare Tax Regimes NowInterest Rates: RLLR vs MCLR vs Fixed

Home loan interest rates in India are benchmarked to either MCLR, RLLR, or are fixed. Most experts now favor RLLR (Repo Linked Lending Rate) because it is directly linked to the RBI's repo rate, offering faster transmission of rate cuts and greater transparency.

| Feature | RLLR (Best) | MCLR | Fixed Rate |

|---|---|---|---|

| Rate Adjustment | Immediate (quarterly) | Slow (1-3 months lag) | Never changes |

| Transparency | High (tied to RBI repo) | Moderate | Fixed upfront |

| Current Range | 8.5-9.0% | 8.75-9.25% | 9.5-10.5% |

| Best For | Long-term borrowers | Medium-term loans | Rate hike protection |

Rates updated Feb 2026. Final rates depend on CIBIL score, loan amount, and customer profile.

Top 5 Home Loan Banks in India (Updated Feb 2026)

| Bank | Interest Rate | Processing Fee | Max Tenure | Best For |

|---|---|---|---|---|

| SBI | 8.50%* | ₹10,000 | 30 years | Govt employees, low rates |

| HDFC | 8.60%* | 0.50% of loan | 30 years | High CIBIL (750+), premium service |

| ICICI | 8.75%* | 0.50% of loan | 30 years | Quick processing, digital experience |

| Axis Bank | 8.75%* | ₹10,000 | 30 years | Salaried professionals, online approval |

| LIC Housing | 8.40%* | 0.25% of loan | 30 years | Lowest rates, flexible tenure |

*Rates as of Feb 2026. Subject to change. Final rates depend on CIBIL score, loan amount, and relationship with bank.

Compare these banks instantly with our calculator:

Compare Bank EMIs NowStamp Duty & Registration Costs by State

Beyond the home loan, you must pay stamp duty and registration charges at the time of property purchase. These vary significantly by state and can add 5-8% to your total property cost. This is a one-time cost paid to the state government.

| State | Stamp Duty (Men) | Stamp Duty (Women) | Registration Charge |

|---|---|---|---|

| Maharashtra (Mumbai) | 5-6% | 4% | 1% |

| Delhi | 6% | 4% | 1% |

| Karnataka (Bangalore) | 5% | 3% | 1% |

| Tamil Nadu (Chennai) | 7% | 7% | 1-4% |

| Telangana (Hyderabad) | 5% | 5% | 0.5-1% |

| Gujarat (Ahmedabad) | 4.9% | 4.9% | 1% |

| Uttar Pradesh (Noida) | 7% | 6% | 1% |

| West Bengal (Kolkata) | 6-7% | 6-7% | 1% |

Cost Calculation Example

Property in Mumbai valued at ₹1 Crore:

| Stamp Duty (Male) | ₹6,00,000 |

| Stamp Duty (Female owner) | ₹4,00,000 (Save ₹2L!) |

| Registration Charge | ₹1,00,000 |

| Total (Male) | ₹7,00,000 |

| Total (Female) | ₹5,00,000 |

Tax Saving Hack: Register the property in a female family member's name where applicable to save 1-2% on stamp duty (₹1-2 lakhs on a ₹1 crore property). Ensure she meets co-ownership and loan eligibility criteria.

Smart Prepayment Strategy

Making part prepayments on your home loan can save you lakhs in interest and reduce your loan tenure significantly. Since floating rate loans have ZERO prepayment penalties (RBI mandated), you should consider regular prepayments whenever you have surplus funds.

Pay a lump sum amount towards your loan while continuing regular EMIs. You can choose to either:

- Reduce tenure: Keep EMI same, finish loan faster

- Reduce EMI: Keep tenure same, lower monthly burden

Recommended: Reduce tenure for maximum interest savings

Pay the entire outstanding principal amount and close the loan completely. This eliminates all future interest payments.

- No penalty: On floating rate loans

- Property released: Bank removes mortgage lien

Note: Fixed-rate loans may charge 2-4% penalty

Loan Details

- Loan Amount: ₹50 Lakh

- Interest Rate: 8.5% p.a.

- Tenure: 20 years

- EMI: ₹43,391/month

Scenario: ₹5 Lakh prepayment after 5 years

| Option | New Tenure | Total Interest Saved |

|---|---|---|

| Without Prepayment | 20 years | - |

| With Prepayment (Reduce Tenure) | 14 years | ₹12,50,000 |

A ₹5L prepayment saves you ₹12.5L in interest and reduces tenure by 6 years!

Early Years (First 10 years)

Maximum interest savings since 70-80% of EMI goes towards interest. Even small prepayments have huge impact.

When You Get Windfall Income

Annual bonus, inheritance, sale of investments - use 50-70% towards prepayment instead of new purchases.

Don't Prepay If...

You have high-interest debt (credit cards, personal loans) - pay those first. Or if you're claiming maximum tax benefits and in 30% bracket.

Calculate your prepayment impact: Use our prepayment calculator to see exact savings based on your loan details.

Why Home Loan Applications Get Rejected

Understanding common rejection reasons helps you prepare better and avoid application denials. Here are the top reasons banks reject home loan applications and how to fix them.

1. Low CIBIL Score (Below 650)

Most common rejection reason. Banks view low scores as high credit risk.

Solution: Wait 6-12 months, pay all dues on time, reduce credit utilization below 30%, correct errors in CIBIL report, avoid multiple loan inquiries.

2. High FOIR (Above 60%)

Too many existing loans eating into your income. Bank doubts your repayment capacity.

Solution: Close small personal loans, pay off credit card debt, add co-applicant with income, apply for lower loan amount, wait for salary increment.

3. Property Legal Issues

Unclear title, pending litigation, unapproved construction, or property in restricted zones.

Solution: Get legal opinion from property lawyer before applying, ensure encumbrance certificate is clear, verify builder's credentials and approvals, choose properties in bank-approved projects.

4. Insufficient or Inconsistent Income Proof

Self-employed with fluctuating income, cash-based business, or incomplete ITR filings.

Solution: File ITR regularly for 3 years, maintain proper business accounts, show consistent profit trends, get CA-certified financial statements, provide GST returns if applicable.

5. Job Instability or Frequent Job Changes

Less than 2 years in current job, multiple job switches in short period, or working in unstable industry.

Solution: Wait until you complete 2 years in current organization, provide strong employment continuity letter, show salary growth trajectory, apply through employer tie-ups for better approval chances.

6. Age Factor (Too Young or Too Old)

Below 25 years with limited work experience or above 55-60 years nearing retirement.

Solution: Add younger co-applicant if you're near retirement, choose shorter tenure, provide additional income sources (rent, business), opt for lower loan amount with higher down payment.

Pro Tip: If your application gets rejected, wait at least 3-6 months before reapplying. Use this time to fix the issues mentioned above. Multiple rejections in short period further damage your credit score.

Borrower Profile

Annual Tax Savings Breakdown (Old Tax Regime)

| Principal Repayment (80C) | ₹1,50,000 |

| Interest Payment (24b) | ₹2,00,000 |

| Total Deduction | ₹3,50,000 |

| Tax Saved (30% bracket) | ₹1,05,000/year |

Over 20 years, Amit saves ₹21 lakhs in taxes while building ₹50L+ equity in his property!

Total Cost Breakdown

| Loan Principal | ₹50,00,000 |

| Total Interest Paid (20 years) | ₹54,13,840 |

| Processing Fees (0.5%) | ₹25,000 |

| Stamp Duty & Registration (6%) | ₹6,00,000 |

| Total Cost | ₹1,10,38,840 |

| Minus Tax Savings (20 years) | - ₹21,00,000 |

| Effective Cost | ₹89,38,840 |

Buy vs Rent: Which Makes Financial Sense?

One of the most critical financial decisions in your 20s-30s is whether to buy a home or continue renting. The answer depends on multiple factors including your career stability, city of residence, and financial goals.

Ownership & Equity Building

Property becomes yours after tenure. Build ₹50L+ equity

Tax Benefits

Save ₹1-2L/year under old regime (80C + 24b)

Forced Savings

EMI acts as disciplined wealth creation

Appreciation Potential

Property values grow 5-8% annually in good locations

Low Flexibility

Can't move easily for job opportunities

Maintenance Costs

Property tax, society charges, repairs add up

High Flexibility

Move cities for better jobs or lifestyle

Lower Upfront Cost

No 10-25% down payment needed

HRA Tax Benefit

Deduct 50% of rent (metro) or 40% under 80GG

No Maintenance Hassle

Owner handles repairs and society issues

No Ownership

Rent is pure expense, no equity building

Rent Increases

Landlord can hike rent 10-15% every 2-3 years

✅ Buy If...

- Settled in one city for 7+ years

- Stable job/business with good income

- Can afford 20-30% down payment

- EMI-to-income ratio below 40%

- Want to build long-term wealth

- Can claim tax benefits (old regime)

🤔 Rent If...

- Job requires frequent city changes

- Early in career (first 3-5 years)

- Can't afford 20% down payment

- Rent-to-EMI ratio is less than 50%

- Prefer flexibility over stability

- Want to invest in higher-return assets

💡 Smart Strategy: Rent Where You Live, Own Where You Can

If you work in expensive metros like Mumbai or Bangalore, consider renting in the city while buying property in your hometown or Tier-2 city. This gives you rental income from owned property while maintaining job flexibility. Many NRIs and young professionals follow this model successfully.

Frequently Asked Questions

Ready to Calculate Your Home Loan EMI?

Use our advanced home loan calculator to instantly find your EMI, total interest, and eligibility based on your income and credit score. Compare multiple banks in one place.

Calculate My Home Loan NowFree • No registration required • Instant results

- CIBIL score of 750+ gets you the best interest rates (8.5-8.75%). Work on improving your credit score before applying.

- Tax benefits up to ₹3.5 lakh/year are available only under the old tax regime (Sections 80C and 24b). Calculate which regime suits you better.

- RLLR-linked loans offer better transparency and faster rate adjustments compared to MCLR. Most experts recommend floating over fixed rates.

- Prepayment in early years saves maximum interest since 70-80% of initial EMI goes towards interest. No penalty on floating rate loans.

- Joint home loans with co-owners can double your tax benefits to ₹7 lakh/year if both borrowers are in the 30% tax bracket.

- Stamp duty varies by state (4-7%) and is lower for women in several states. Factor this 5-8% additional cost into your budget.

- Keep FOIR below 50-60% by closing unnecessary loans before applying. High FOIR is a major rejection reason.

Written by Fincado Research Team

Expert financial analysts specializing in personal finance, home loans, and tax planning for Indian consumers.

Found this guide helpful? Share it with friends planning to buy a home:

Disclaimer

This guide is for informational purposes only and should not be considered financial advice. Home loan interest rates, eligibility criteria, and tax laws are subject to change. Section 80EEA benefits expired on March 31, 2022, and are no longer available. Please consult with a certified financial advisor or chartered accountant before making any financial decisions. Actual loan approval and terms depend on individual circumstances, bank policies, and credit profile. Information last updated: Feb 2026.