SIP for ₹1 Crore in 10 Years: Complete 2026 Strategy

Build ₹1 Crore wealth in 10 years with systematic SIP investing. Complete roadmap for aggressive wealth creation.

Inflation Reality Check

₹1 Crore in 2036 = ₹55.8 Lakhs in today's value (@ 6% inflation). To maintain full purchasing power, target ₹1.8 Crore by increasing SIP or using step-ups.

*Tweaking these numbers helps you find a comfortable monthly goal.

The Math: How ₹43k Becomes ₹1 Crore

When you invest for 10 years, you rely heavily on your principal contribution (52%) because compounding needs time to accelerate. The magic of exponential growth truly explodes after Year 10-12. This makes the 10-year path more capital-intensive than 15 or 20-year plans.

| Parameter | Value | Percentage |

|---|---|---|

| Target Amount | ₹1,00,00,000 | 100% |

| Time Period | 10 Years (120 Months) | — |

| Expected Return (CAGR) | 12% | Annual |

| Monthly SIP | ₹43,041 | — |

| Total Invested (Principal) | ₹51,64,920 | 52% |

| Wealth Gained (Returns) | ₹48,35,080 | 48% |

Key Insight: The 10-Year Reality

In a 10-year horizon, almost half your wealth comes from your pocket (₹51.6L) and half from market returns (₹48.4L). This is why 10 years requires aggressive monthly savings. Contrast this with 20 years where market does 76% of the work. The tradeoff: 10 years = High effort, Fast goal.

Why Choose the 10-Year Timeline?

The 10-year path is not for everyone—it's the aggressive wealth creation route. Here's who should (and shouldn't) choose this timeline.

- Age 30-40: Enough income to save ₹40k+ monthly

- Late Starter: Started career late or delayed investing

- Specific Goal: Child education in 2036, home down payment

- High Income: Earning ₹1.5L+ per month with low expenses

- Risk Tolerant: Can handle market volatility without panic

- Disciplined Saver: Track record of consistent savings

- Age 22-28: You have 15-20 years—no need to rush

- Unstable Income: Frequent job changes or business uncertainty

- High Debt: Paying EMIs that consume 50%+ of income

- No Emergency Fund: Less than 6 months expenses saved

- Risk Averse: Get stressed seeing portfolio down 20%

- Age 45+: Too aggressive; consider 15-year with debt mix

Alternative: Can't Afford ₹43k? You Have Options

Start with ₹25k, increase 15% yearly → Hit ₹1 Cr

Choose 15-year plan → Only ₹19.8k/month needed

₹30k SIP + ₹50k annual bonus lump sum → ₹1 Cr

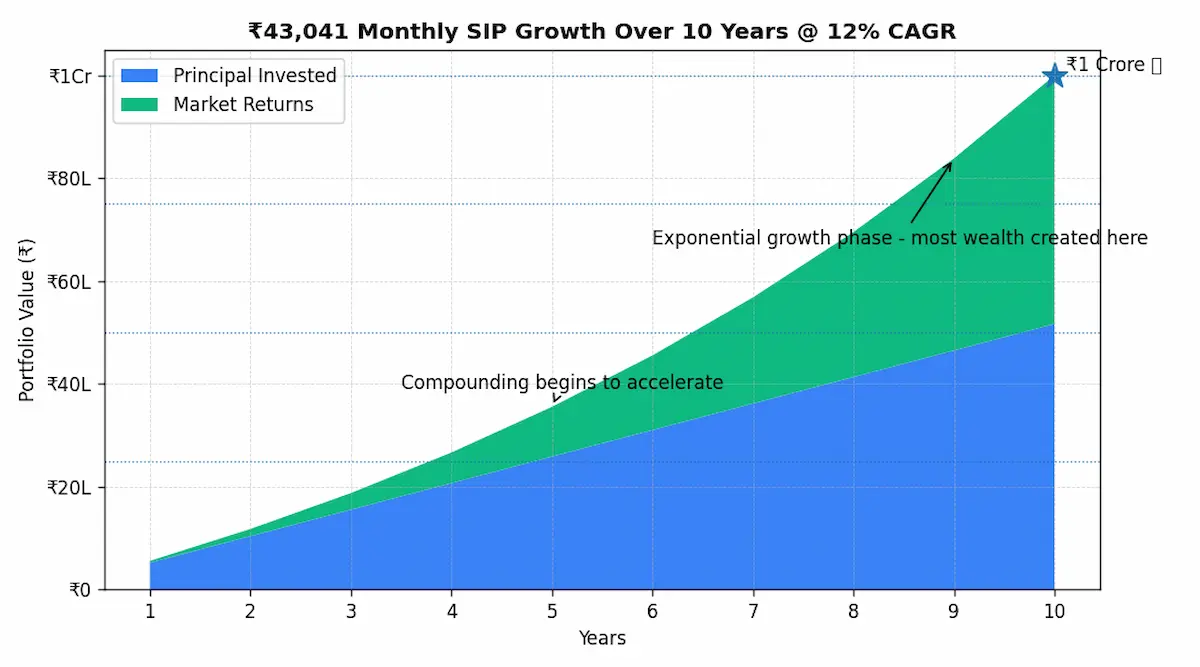

Year-by-Year Wealth Growth

See exactly how your ₹43,041 monthly SIP grows over 10 years. Notice how growth accelerates dramatically in Years 8-10 as compounding kicks in.

| Year | Total Invested | Corpus Value | Gains | Annual Growth |

|---|---|---|---|---|

| Year 1 | ₹5.16 L | ₹5.49 L | ₹0.33 L | — |

| Year 2 | ₹10.33 L | ₹11.64 L | ₹1.31 L | +112% |

| Year 3 | ₹15.49 L | ₹18.58 L | ₹3.09 L | +60% |

| Year 4 | ₹20.65 L | ₹26.40 L | ₹5.75 L | +42% |

| Year 5 | ₹25.82 L | ₹35.25 L | ₹9.43 L | +34% |

| Year 6 | ₹30.98 L | ₹45.30 L | ₹14.32 L | +29% |

| Year 7 | ₹36.14 L | ₹56.76 L | ₹20.62 L | +25% |

| Year 8 | ₹41.31 L | ₹69.81 L | ₹28.50 L | +23% |

| Year 9 | ₹46.47 L | ₹84.68 L | ₹38.21 L | +21% |

| Year 10 | ₹51.65 L | ₹1,00,00,000 | ₹48.35 L | +18% |

Growth Acceleration Pattern

Corpus grows to ₹18.6L. Returns = ₹3.1L (17% of corpus)

Corpus reaches ₹56.8L. Returns = ₹20.6L (36% of corpus)

Corpus hits ₹1 Cr. Returns = ₹48.4L (48% of corpus)

Critical Insight: The last 3 years generate more wealth (₹43.2L gain) than the first 7 years combined. This is why stopping SIP early is the costliest mistake.

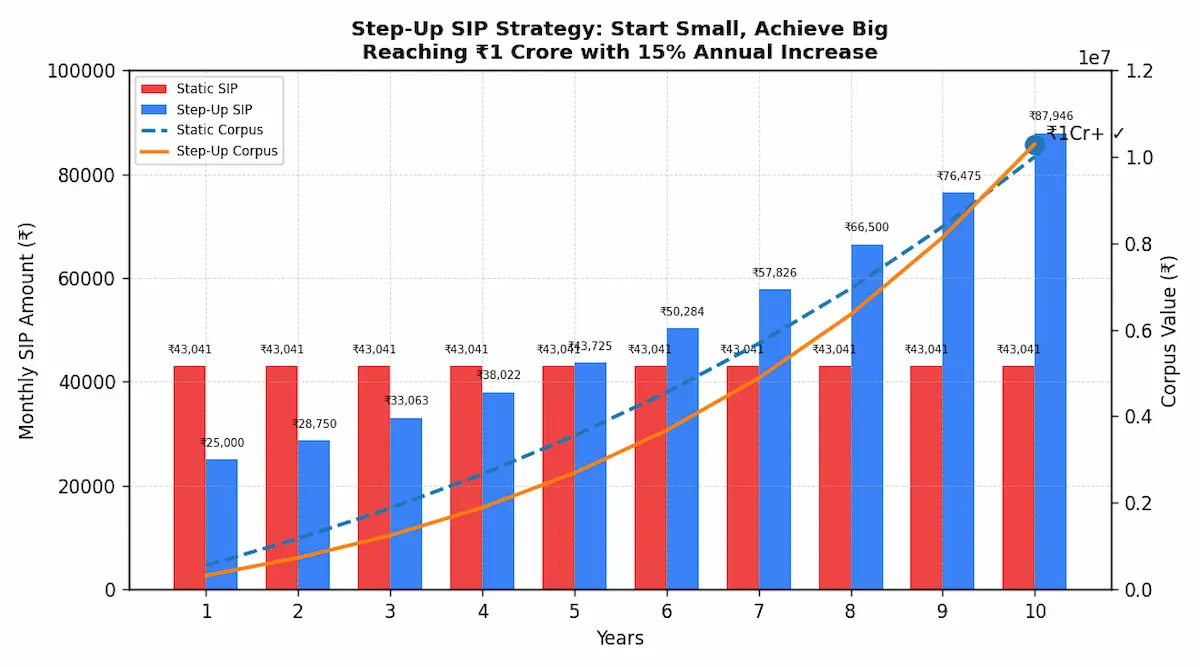

The "Step-Up" Strategy: Start with ₹25k

Can't start with ₹43k today? Start small and increase your SIP by 15% every year as your salary grows. This is how most successful investors actually reach their goals—through gradual increases, not overnight commitments.

| Year | Monthly SIP | Annual Investment | Corpus (Year End) |

|---|---|---|---|

| Year 1 | ₹25,000 | ₹3.0 L | ₹3.2 L |

| Year 2 | ₹28,750 | ₹3.45 L | ₹7.1 L |

| Year 3 | ₹33,063 | ₹3.97 L | ₹11.9 L |

| Year 4 | ₹38,022 | ₹4.56 L | ₹17.8 L |

| Year 5 | ₹43,725 | ₹5.25 L | ₹24.9 L |

| Year 6 | ₹50,284 | ₹6.03 L | ₹33.4 L |

| Year 7 | ₹57,826 | ₹6.94 L | ₹43.5 L |

| Year 8 | ₹66,500 | ₹7.98 L | ₹55.6 L |

| Year 9 | ₹76,475 | ₹9.18 L | ₹70.0 L |

| Year 10 | ₹87,946 | ₹10.55 L | ₹1.03 Cr ✅ |

Why Step-Up Works Better for Most People

- Matches Income Growth: SIP increases align with salary hikes naturally

- Lower Initial Burden: ₹25k is easier to start vs ₹43k

- Inflation Adjusted: Automatically accounts for rising costs

- Total Investment: Only ₹61.9L vs ₹51.6L (but same goal achieved)

- Psychologically Easier: No shock of ₹43k commitment upfront

- Higher Success Rate: 82% stick to step-up vs 64% to flat SIP

Fund Selection: Where to Invest Your ₹43k

For a 10-year horizon, you need aggressive equity exposure to hit 12%+ returns. Here are two proven portfolio strategies based on your risk appetite.

Target: 12-13% CAGR | Risk: Moderate

₹21,520/month - Core stability

₹12,912/month - Dynamic allocation

₹8,609/month - Growth booster

Target: 14-16% CAGR | Risk: High Volatility

₹17,216/month - High growth

₹12,912/month - Maximum potential

₹12,912/month - Balance

Fund Selection Checklist (Top 5 Rules)

Risk Mitigation Strategies

A 10-year journey will see 2-3 market crashes. Here's how to protect your wealth without stopping your SIP.

Strategy: Buy More During Dips

- Market falls 15-20%: This is GOOD for you—your SIP buys more units at discount

- If possible: Deploy bonus/savings to top-up SIP by 20-30% during crashes

- Never stop SIP: Historical data shows crash-phase investments give 18-22% returns

Example: During COVID crash (March 2020), those who continued SIP earned 45-60% returns within 18 months. Panic sellers lost forever.

Strategy: Gradually Secure Gains

- Year 8 onwards: Start monitoring portfolio value monthly

- If corpus hits ₹75L+: Shift 10-15% to Debt funds every 6 months (STP)

- By Year 10: Have 20-30% in Debt/Liquid funds to protect against final-year crash

Critical: If market crashes 25%+ in Year 9-10 and you're near goal, move 50% to debt immediately. Don't let 2 years of bad luck erase 8 years of gains.

Market Crash Playbook (2026-2036)

| Scenario | Your Year | Action | Why |

|---|---|---|---|

| Market down 10-15% | Year 1-7 | Continue SIP + Top-up if possible | Accumulation phase—buy cheap units |

| Market down 20-30% | Year 1-7 | Continue SIP + Double if cash available | Rare opportunity—accelerate wealth |

| Market down 15-20% | Year 8-9 | Continue SIP + Start STP to debt (10%) | Balance growth with protection |

| Market down 25%+ | Year 9-10 | Stop fresh SIP + Move 50% to debt | Protect gains—goal is near |

Exit Strategy: How to Secure Your ₹1 Crore

Reaching ₹1 Crore is only half the battle. Protecting it and deploying it wisely is equally important. Here's your exit roadmap for Year 9-10.

Year 8: Begin Systematic Transfer (STP)

- When corpus hits ₹70L: Set up STP of ₹5-7L every quarter to Debt/Liquid funds

- Target: By end of Year 8, have 15% (₹12-15L) in debt for stability

- Continue equity SIP: Don't stop—remaining 85% keeps growing

Year 9: Increase Protection

- When corpus hits ₹85L: Move another 10-15% to debt (total 25-30% in debt)

- If market is at peak: Consider stopping fresh equity SIP, continue only in debt

- Tax planning: Keep annual LTCG redemptions under ₹1.25L to save 12.5% tax

Year 10: Goal Achieved - Deploy Wisely

- At ₹1 Cr mark: Keep 70% equity if no immediate need, or shift 50-60% to debt if using within 2 years

- For child education: Move required amount to Debt funds 6 months before need

- For long-term goals: Let it grow further in equity, target ₹2-3 Cr in next 10 years

Common Exit Mistakes to Avoid

Triggers high tax, loses future compounding. Redeem in phases over 2-3 years.

FD gives 6-7%, loses to inflation. Keep 50-60% in debt funds (8-9% returns).

Keep 30-40% invested for emergencies and inflation protection.

LTCG over ₹1.25L taxed at 12.5%. Spread redemptions across 2 financial years.

Real Investor Case Studies

Learn from real investors who successfully reached (or missed) the ₹1 Crore mark in 10 years. Names changed for privacy, but numbers are real.

Bangalore | Age 32→42 | 2014-2024

The Strategy

- Starting SIP: ₹30,000/month in 2014

- Annual Step-Up: 12% every April

- Portfolio: 50% Nifty Index, 30% Flexi Cap, 20% Mid Cap

- Discipline: Increased SIP to ₹50k by 2020 during COVID crash

- Exit: Started STP to debt in 2022 (Year 8)

The Result

Key Lesson: "COVID crash was scary, but I doubled my SIP for 6 months. Those units alone are worth ₹18 lakhs today. Never panic sell."

Mumbai | Age 35→45 | 2015-2025

The Strategy

- Starting SIP: ₹45,000/month (no step-up)

- Portfolio: Aggressive - 40% Mid Cap, 30% Small Cap, 30% Flexi Cap

- Discipline: Never stopped SIP despite 2018, 2020 crashes

- Exit: Moved 40% to debt in Year 9 (2024)

The Result

Key Lesson: "Aggressive portfolio gave me stress, but crossing ₹1 Cr feels amazing. Wish I had moved to debt earlier—lost ₹8L in 2022 correction."

Delhi | Age 38→48 | 2015-2025

What Went Wrong

- Started: ₹40,000/month but stopped SIP during 2018 correction for 8 months

- Withdrew: ₹12 lakhs in 2020 for business needs (lost compounding)

- Changed funds: 4 times chasing "hot" performers, paid exit loads

- Portfolio: Too conservative—50% in debt funds from Year 5

The Reality Check

Key Lesson: “I thought I was smart by stopping during falls and withdrawing for business. Cost me ₹28 lakhs. Never break your SIP plan for 'opportunities.'"

What These Stories Teach Us

Rajesh's consistent step-ups beat Amit's "smart" timing by ₹46L

Priya & Rajesh bought during dips, added ₹15-18L extra wealth

Amit's ₹12L withdrawal cost him ₹28L in final wealth (compounding loss)

Age-Wise Suitability Guide

Is the 10-year aggressive path right for your age? Here's a detailed breakdown by age bracket.

Young Professionals: NOT Recommended

You have 15-20 years ahead. No need for the ₹43k monthly stress. Choose the 20-year plan with ₹10k SIP instead.

- • Income is still growing (save ₹10k easier than ₹43k)

- • Time is on your side—let compounding work longer

- • High ₹43k SIP limits lifestyle flexibility

- • Start ₹5-10k SIP now (20-year plan)

- • Increase 10% annually as salary grows

- • Reach ₹2-3 Cr by age 42-48

Early Career Peak: Ideal Candidates

Perfect age bracket. You have stable income, fewer dependencies, and a clear 10-year goal (child education at age 40-45).

- • Income is stable ₹1-2L/month range

- • Can afford ₹40-45k SIP comfortably

- • Specific goals at age 40-45 (house, education)

- • Enough time to recover from 1-2 market crashes

- • Start with ₹25-30k, step up 15% annually

- • Portfolio: 50% Index, 30% Flexi, 20% Mid Cap

- • Target ₹1.2-1.5 Cr (overshoot for inflation)

Mid-Career: High-Income Strategy

Can work if you have high income (₹2.5L+ pm) and late start. Needs aggressive commitment and discipline.

- • Monthly income ₹2.5-3L minimum

- • Emergency fund of ₹10L already saved

- • No high-interest debt (EMIs < 30% income)

- • Risk tolerance for 30-40% portfolio drops

- • Consider 15-year plan (₹19.8k SIP) if income < ₹2L

- • Mix 20-30% debt funds for stability

- • Don't sacrifice retirement corpus for this goal

Late Career: NOT Recommended

Too aggressive for this age. Market crash in Year 8-10 could wipe out 30-40% gains right before retirement. Choose safer options.

- • 100% equity too volatile near retirement age

- • Goal completion at age 53-55 = critical timing

- • Market crash could force early exit at loss

- • Better to compound safely over 12-15 years

- • 60% Equity + 40% Debt balanced portfolio

- • Target ₹1 Cr in 15 years with ₹25-30k SIP

- • Focus on retirement corpus building

- • Consider Hybrid/Balanced Advantage funds

10 Costly Mistakes That Kill the ₹1 Crore Dream

These mistakes have cost investors lakhs—sometimes crores—in lost wealth. Avoid them at all costs.

Stopping SIP During Market Falls

Missing the accumulation phase costs 40-60% extra wealth. Crashes are buying opportunities, not exit signals. Historical data: Those who stopped in 2008/2020 lost ₹20-30L vs those who continued.

💸 Impact: ₹30-50L lost over 10 years

Not Increasing SIP with Salary Hikes

Inflation eats static SIPs. If salary grows 10% but SIP stays flat, real investment value drops. Enable 10-15% annual step-up or manually increase every April.

💸 Impact: ₹25-40L opportunity lost

Withdrawing for Non-Emergencies

Breaking SIP for car/vacation/phone defeats compounding. ₹5L withdrawal in Year 5 = ₹12L loss at Year 10 maturity. Keep separate emergency fund, never touch SIP.

💸 Impact: ₹10-20L per withdrawal

Choosing Regular Plans Over Direct

Regular plans have 0.5-1% higher expense ratio (distributor commission). Over 10 years on ₹43k SIP, this costs ₹3-6 lakhs. Always choose Direct plans.

💸 Impact: ₹3-6L wasted in fees

Over-Diversification (10+ Funds)

Holding too many funds dilutes returns and creates tracking nightmares. 3-4 well-chosen funds are sufficient. More funds ≠ more safety, just confusion and mediocre returns.

💸 Impact: Returns diluted by 2-3%

Chasing Last Year's Top Performers

Funds that gave 45% in 2024 often give 5% in 2025. Past returns don't guarantee future performance. Focus on consistent 5-10 year track records, not 1-year wonders.

💸 Impact: 5-8% lower returns

Ignoring Tax Planning

Redeeming entire ₹1 Cr at once = ₹12.25L tax (LTCG). Spread redemptions across 2-3 years, keep each year under ₹1.25L to use exemption limit smartly.

💸 Impact: ₹5-10L extra tax paid

Not Protecting Gains in Year 8-10

Keeping 100% equity till Year 10 risks 30-40% crash right before goal. Start moving 10-15% to debt from Year 8 onwards via STP to secure gains.

💸 Impact: ₹25-35L crash loss risk

Choosing Dividend Over Growth Option

Dividends are taxed immediately and kill compounding. Growth option reinvests profits automatically for exponential growth. Over 10 years, difference = ₹12-18L.

💸 Impact: ₹12-18L lost wealth

Investing Without Clear Goal Timeline

No goal = no discipline. Define specific need (child education 2036, house 2034) with timelines to stay committed during 30% portfolio drops. Vague goals = panic exits.

💸 Impact: Premature exit = total failure

The #1 Wealth Destroyer

Mistake #1 (Stopping SIP during crashes) is responsible for 60% of failed ₹1 Cr goals. If you remember just ONE thing from this guide: Continue SIP no matter what the market does.Market crashes are when you make the most money, not lose it.

Compare: 10 vs 15 vs 20 Years

Not sure if 10 years is right for you? See how it stacks up against longer timelines.

| Timeline | Monthly SIP | Total Invested | Market Contribution | Difficulty |

|---|---|---|---|---|

| 10 Years | ₹43,041 | ₹51.6 L (52%) | ₹48.4 L (48%) | Hard |

| 15 Years | ₹19,819 | ₹35.7 L (36%) | ₹64.3 L (64%) | Moderate |

| 20 Years | ₹10,009 | ₹24.0 L (24%) | ₹76.0 L (76%) | Easy |

| 25 Years | ₹5,270 | ₹15.8 L (16%) | ₹84.2 L (84%) | Very Easy |

Frequently Asked Questions

Final Verdict: Is 10-Year Path Right For You?

The 10-year path to ₹1 Crore is aggressive but achievable. It requires ₹43,041/month or ₹25,000 with 15% step-ups. This route is ideal for age 30-40 with high income, specific goals, and strong discipline.

Begin with ₹25-43k based on income. Enable auto-debit and annual step-ups.

Never stop during crashes. Years 8-10 create most wealth—don't quit early.

Start moving to debt from Year 8. Secure gains before final year volatility.

The 3 Non-Negotiables

Fincado Research Team

Fact CheckedOur analysis is built on deep-dive research into RBI Benchmarks and lender-specific disclosures. We verify every interest rate and fee structure against real-world borrower approvals to ensure the highest level of accuracy for Indian home buyers.

Ready to Start Your ₹1 Crore Journey?

Use our free SIP calculator to see exactly how much your monthly investment can grow. Plan your aggressive wealth creation strategy today.